The next big leap in African commerce is not happening in a bank branch. It is happening in taxis, open markets, small kiosks, mobile apps, and merchant dashboards, where digital payments are becoming the default way people move money, buy goods, and run businesses.

That shift matters because Africa is not just adopting digital finance, it is helping define what the future of payments looks like in markets with fragmented infrastructure, rising mobile usage, and intense demand for faster, cheaper transactions. In other words, the continent is not following the global payments playbook, it is rewriting it.

Introduction

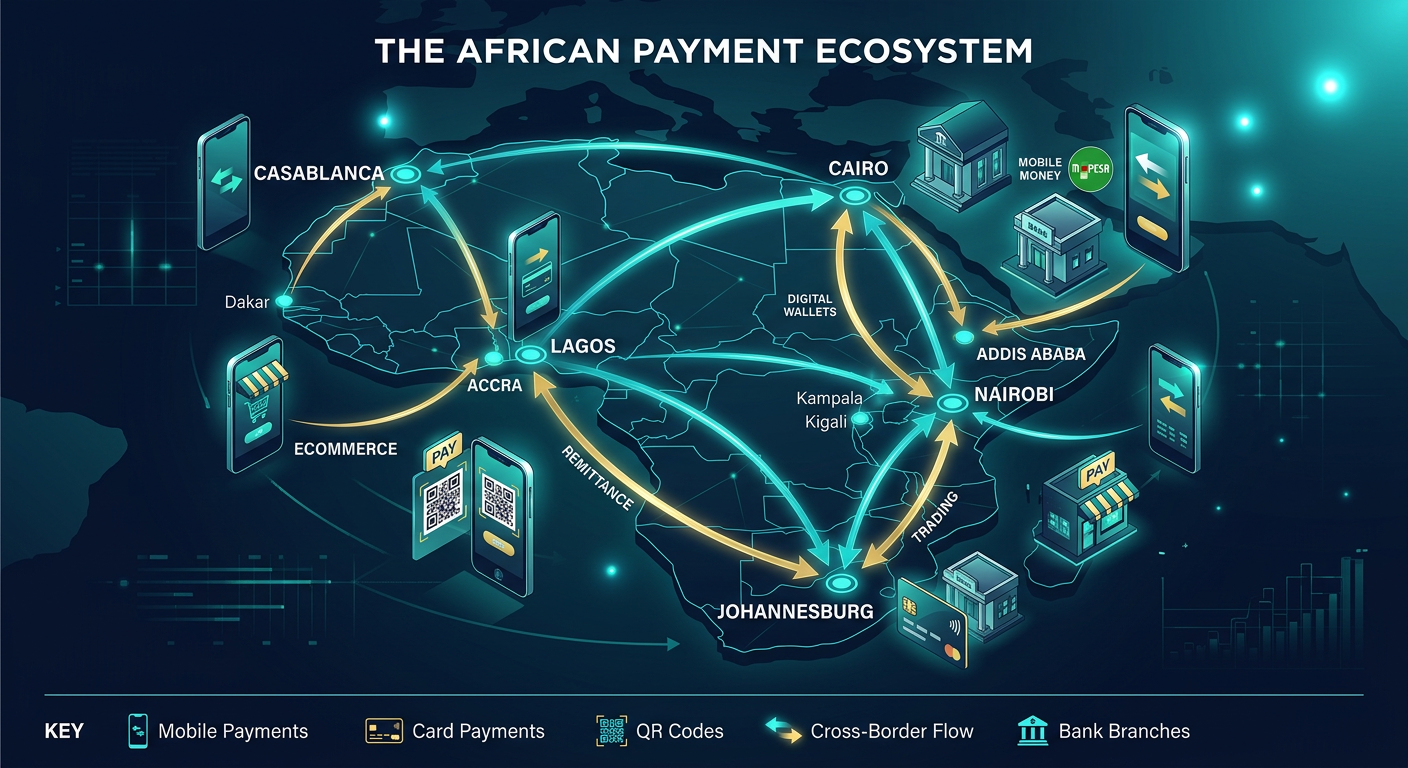

If you want to understand where commerce is headed, watch how people pay. Across Africa, the future of digital payments is being shaped by mobile money, bank transfers, QR codes, agency banking, payment gateways, and new cross-border rails that are designed for a continent with many currencies and many payment habits.

The opportunity is enormous. GSMA data shows Africa remains the center of global mobile money activity, while the African Development Bank has also emphasized the need for broader digital access and payment infrastructure to deepen inclusion. TechCity’s own reporting has repeatedly shown how local players like Moniepoint, Flutterwave, Zone, Hizo, and others are pushing the market forward with tools for merchants, consumers, and cross-border trade. (gsma.com)

Why the Next Phase Will Look Different

The first phase of Africa’s payments story was about getting people into the system. The next phase is about making that system invisible, instant, and interoperable.

1. Mobile money will keep expanding, but with more sophistication

Mobile money has moved beyond person-to-person transfers. It is now a utility for bills, savings, merchant payments, lending, and increasingly, business operations. GSMA’s reporting shows Africa remains the world leader in mobile money usage and transaction volume, which means future growth will be less about proving the model and more about improving speed, reliability, and interoperability. (gsma.com)

2. Interoperability will decide the winners

People do not want to ask, “Which app do you use?” They want to pay and move on. That is why the most valuable payment platforms will be the ones that connect banks, wallets, cards, agents, and merchants without friction. TechCity’s coverage of Zone’s blockchain-based payment gateway and Collect Africa’s multi-channel payment tools points to the same trend: the future belongs to infrastructure that connects everything instead of isolating users inside one network. (techcityng.com)

3. Cross-border payments will become a major battleground

Africa’s trade story has always been held back by currency fragmentation, expensive FX conversion, and settlement delays. That is why cross-border payment products are becoming central to fintech strategy. TechCity reported on Flutterwave and Yellow Card joining the Circle Payments Network, and on Hizo building tools for intra-Africa payments in local currencies, both of which reflect the growing demand for faster regional settlement. (techcityng.com)

What Is Driving Adoption

Several forces are pushing digital payments deeper into everyday life.

Smartphone growth and better connectivity

As more Africans access smartphones and mobile internet, digital wallets and payment apps become easier to use. The GSMA notes that mobile technologies continue to contribute significant economic value across the continent, which supports wider adoption of mobile-first financial services. (gsma.com)

Merchant demand for speed and record keeping

For SMEs, digital payments are about more than convenience. They improve cash tracking, reduce theft risk, and make it easier to qualify for credit. That is part of why platforms like Moniepoint have become so important to small businesses across Africa. (techcityng.com)

Consumer expectations are changing

Younger users increasingly expect instant payment confirmation, low fees, and simple interfaces. Once someone gets used to paying in one tap or transferring money in seconds, cash starts to feel slow. That behavioral shift is hard to reverse.

The Biggest Opportunities Ahead

The future of digital payments in Africa is not only about convenience. It opens real economic doors.

Financial inclusion at scale

Millions of people still operate outside formal banking, but digital rails can bring them in through wallets, agents, and low-cost payment products. The African Development Bank, Mastercard, and the World Bank have all highlighted the importance of expanding digital access and payment options across the region. (afdb.org)

Better credit and business data

Digital payments create transaction histories. Transaction histories create underwriting signals. That means more people and small businesses can access loans, insurance, and savings products based on real activity instead of weak paperwork. This is one reason fintech products are increasingly merging payments with lending and business management tools. (techcityng.com)

More efficient trade across Africa

If payments become easier across borders, trade gets easier too. That matters for importers, exporters, freelancers, creators, and SMEs that sell beyond one national market. The most exciting payment products in Africa are not just local, they are regional by design. (techcityng.com)

The Challenges That Could Slow Progress

The outlook is strong, but the road is not frictionless.

Fragmented regulation

Different licensing rules, settlement regimes, and compliance requirements can slow scale. Fintechs operating across multiple countries often spend heavily on legal, technical, and regulatory adaptation.

Fraud and trust issues

As payment usage grows, fraud grows with it. Consumers and merchants need stronger authentication, better dispute resolution, and clearer security standards to keep trust intact.

Cash will not disappear overnight

Africa is not a one-speed market. In many places, cash remains practical, familiar, and resilient. The future is not a sudden cashless switch, it is a gradual shift toward hybrid systems where cash, cards, mobile money, and bank transfers coexist.

What Businesses Should Do Now

If you are a founder, SME owner, or product builder, the message is simple, build for how people actually pay.

Make payments local first, scalable second

Support the methods your customers already use, whether that is bank transfer, wallet, card, QR, or PoS. Then build the backend so you can expand across markets later.

Treat payments as a growth tool

Payments are not just a checkout function. They are acquisition, retention, and data collection. Every successful payment flow can improve conversion and surface insights about customer behavior.

Plan for interoperability and regulation

The winners in this market will not be the loudest brands. They will be the ones that can integrate quickly, comply consistently, and keep the user experience simple.

FAQ

Will cash still matter in Africa in the future?

Yes. Cash will remain relevant for years, especially in informal and low-connectivity markets. But digital payments will continue taking a larger share of everyday commerce.

Which payment method is growing fastest?

Mobile money and account-to-account transfers remain some of the strongest growth areas, especially in markets where smartphones and low-cost transfers are widely used. (gsma.com)

Are cross-border payments finally improving?

Yes, but unevenly. New networks and fintech partnerships are reducing friction, though currency conversion, regulation, and settlement complexity still slow adoption. (techcityng.com)

Why are fintech startups still attracting attention?

Because payments are the entry point to everything else, lending, savings, commerce tools, and identity. That makes the sector strategically important for both consumers and investors. (techcityng.com)

What makes Africa different from other markets?

Africa’s payments future is being built in a highly mobile, multilingual, and multi-currency environment. That forces innovation in ways many mature markets never had to consider.

What should SMEs prioritize first?

They should prioritize reliability, low transaction friction, and methods that match customer behavior. If the payment flow is hard, sales will suffer.

Build for the New Payment Reality

The future of digital payments in Africa is already taking shape, and it is bigger than wallets and card terminals. It is about infrastructure, inclusion, commerce, and the freedom to move money across borders with less friction.

For TechCity readers, the key takeaway is simple, this is one of the continent’s most important growth stories, and the businesses that understand it early will have a serious advantage. If you want more cross-continental tech analysis, startup insights, and practical fintech coverage, visit TechCity for the latest stories shaping Africa’s digital economy.

Conclusion

Africa’s payments future will be defined by interoperability, mobile-first design, and cross-border simplicity. The companies that win will be the ones that make money movement feel invisible, secure, and affordable.

That is good news for consumers, startups, and SMEs alike. Because when payments get easier, everything else, trade, trust, and growth, gets easier too.